Eurozone flash Composite PMI surprisingly declines in April to 48.6 vs. 50.2 estimates

Eurozone's preliminary HCOB Composite PMI unexpectedly declines in April to 48.6. Economists expected the overall business activity to have grown at a moderate pace to 50.2 from 50.7 in March.

The Services PMI contracts at a faster pace to 47.4 vs. 49.8 estimates. In March, the Services PMI arrived at 50.2. Surprisingly, the Manufacturing PMI expanded at a faster pace to 52.2. The data was expected to come in lower at 50.8 from the previous reading of 51.6.

"The Eurozone is facing deepening economic woes from the war in the Middle East, presenting a major headache for policymakers. The conflict has pushed the economy into decline in April, while driving inflation sharply higher. Increasingly widespread supply shortages, meanwhile threaten to dampen growth further while adding more upward pressure to prices in the coming weeks. The war is currently hitting the service sector hardest, where business activity is falling at a rate not seen since the pandemic lockdowns of early 2021," Chris Williamson, Chief Business Economist at S&P Global Market Intelligence:

Market reaction

EUR/USD remains almost steady after the Eurozone PMI data release at around 1.1700 as of writing.

(This section below was added at 07:32 GMT after the release of the German HCOB PMI data for April)

German flash Composite PMI unexpectedly declines in April. According to flash estimates, the Composite PMI contracts to 48.3, while it was expected to expand again, but at a moderate pace to 51.1 from 51.9 in March.

The overall business activity declined as the service sector activity surprisingly contracted. The Services PMI arrives at 46.9 lower than estimates of 50.3 and the previous reading of 50.9. The Manufacturing PMI expands again, but at a moderate pace to 51.2 vs. 51.3 estimates and the prior release of 52.2.

"The recovery in the German economy has been stopped in its tracks by the war in the Middle East. A ten-month sequence of growth came to an end in April as business activity contracted against a backdrop of heightened uncertainty and sharply rising prices," Phil Smith, Economics Associate Director at S&P Global Market Intelligence, said.

Market reaction

No immediate impact on the Euro (EUR) after the German PMI data release. As of writing, EUR/USD trades marginally lower to near 1.1700.

(This section below was published at 05:40 GMT as a preview of the German/Eurozone HCOB PMI data for April)

German/ Eurozone flash PMIs Overview

The preliminary German and Eurozone flash HCOB Purchasing Managers’ Index (PMI) data for April is due for release today at 07:30 and 08:00 GMT, respectively.

Amongst the Euro area economies, the German and the composite Eurozone PMI reports hold more relevance, in terms of their impact on the European currency and the related markets as well.

The flash Composite PMI for Germany is expected to have expanded again, but at a moderate pace due to a slowdown in both the manufacturing and the services sectors. The Composite PMI is seen arriving lower at 51.1 from 51.9 in March.

Germany’s Manufacturing PMI is expected to have fallen to 51.3 from the previous reading of 52.2. Meanwhile, the Services PMI is estimated to have dropped to 50.3 from the prior release of 50.9.

The forecast for the Eurozone flash Composite PMI for April also shows that the overall private sector output expanded at a moderate pace. Eurozone’s manufacturing output growth slowed down, and the services sector activity contracted. A figure below the 50.0 threshold is considered a contraction in the economic activity.

According to preliminary estimates, the Eurozone Composite PMI drops to 50.2 from 50.7 in March. The Manufacturing PMI is seen arriving lower at 50.8 from the prior release of 51.6. The Services PMI is expected to have contracted to 49.8 after slowing down to 50.2 in March.

How could German/ Eurozone flash PMIs affect EUR/USD?

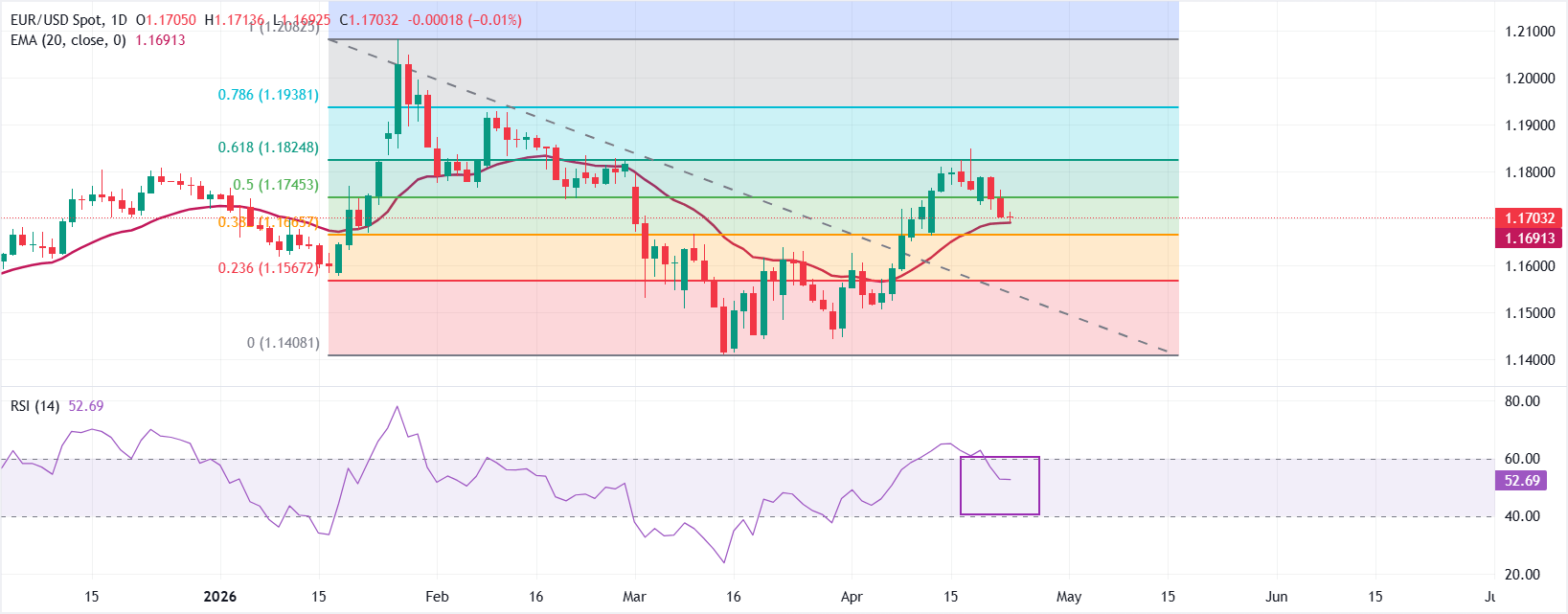

EUR/USD is marginally down to near 1.1700 during the early European trade on Thursday. The pair has corrected to near the 20-period exponential moving average (EMA), which is at 1.1691, but sits north of the 38.2% Fibonacci retracement at 1.1666 of the 1.1408–1.2082 swing, suggesting underlying demand on shallow pullbacks.

The Relative Strength Index (RSI) falls into the 40.00-60.00 zone after failing to hold above the 60.00 level, indicating balanced momentum with an upside bias.

On the topside, initial resistance is located at the 50% Fibonacci retracement at 1.1745; a daily close above this barrier would expose the 61.8% retracement at 1.1825, followed by 1.1938 and the cycle high region near 1.2082. On the downside, immediate support is provided by the 20-period EMA at 1.1691, ahead of the 38.2% retracement at 1.1666; a deeper setback would bring the 23.6% level at 1.1567 into view, with more important structural support down at the 1.1408 swing low.

(The technical analysis of this story was written with the help of an AI tool.)

Euro FAQs

The Euro is the currency for the 20 European Union countries that belong to the Eurozone. It is the second most heavily traded currency in the world behind the US Dollar. In 2022, it accounted for 31% of all foreign exchange transactions, with an average daily turnover of over $2.2 trillion a day. EUR/USD is the most heavily traded currency pair in the world, accounting for an estimated 30% off all transactions, followed by EUR/JPY (4%), EUR/GBP (3%) and EUR/AUD (2%).

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy. The ECB’s primary mandate is to maintain price stability, which means either controlling inflation or stimulating growth. Its primary tool is the raising or lowering of interest rates. Relatively high interest rates – or the expectation of higher rates – will usually benefit the Euro and vice versa. The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.

Eurozone inflation data, measured by the Harmonized Index of Consumer Prices (HICP), is an important econometric for the Euro. If inflation rises more than expected, especially if above the ECB’s 2% target, it obliges the ECB to raise interest rates to bring it back under control. Relatively high interest rates compared to its counterparts will usually benefit the Euro, as it makes the region more attractive as a place for global investors to park their money.

Data releases gauge the health of the economy and can impact on the Euro. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the single currency. A strong economy is good for the Euro. Not only does it attract more foreign investment but it may encourage the ECB to put up interest rates, which will directly strengthen the Euro. Otherwise, if economic data is weak, the Euro is likely to fall. Economic data for the four largest economies in the euro area (Germany, France, Italy and Spain) are especially significant, as they account for 75% of the Eurozone’s economy.

Another significant data release for the Euro is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period. If a country produces highly sought after exports then its currency will gain in value purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.